Every company desires to win profitable customers. The bigger the contract, the higher the margin, the better. And that’s why companies across the board are drawn to “upmarket” customers.

Upmarket customers are the ones that are simultaneously the most demanding and most profitable. As a CEO, upmarket customers are the ones with the biggest problems your company can solve. For that reason, they’re willing to pay you the most for your solutions. They typically have needs that are more complex than much of your base – forcing you to quickly build new capabilities to satisfy them.

When it comes to the world of SaaS, these are the customers with huge MRR. One upmarket customer can make up for a hundred volume customers. They're the logos you put on your website. They're the Global 2000 - businesses that everyone recognizes. You constantly feel their allure as you grow your business.

Figure 1 - Revenue per customer over time (sample public companies)

But, as anyone who has read The Innovator’s Dilemma can remind you, upmarket customers come with their own risks. Listening too exclusively to your most profitable, most demanding, customers often causes companies to build features and distribution models that simply can’t compete over long periods of time. Listening to the demands of these unique customers often provides managers a false sense of confidence that they're headed down the right path.

Over time, upmarket customers unintentionally lead businesses astray - opening the doors to disruption.

For all these reasons, it’s been easy for Venture Capitalists to predict the constant cycle of disruption in technology markets. Not only is technology changing at an ever more rapid pace, but we're also seeing a slew of cloud software vendors march upmarket - increasing their revenue per customer by winning large enterprise contracts. The gut reaction of most observers then is to believe these vendors should be constantly subject to disruption. That's certainly been the sentiment shared by a number of bloggers, investors, and pundits who focus on the software sector.

Unfortunately, it's not quite that simple. And VCs heralding continuous disruption in SaaS should keep that in mind.

There are thousands of ways companies can fall victim to attack by new market entrants. Disruption is a specific one. It also happens to follow a powerful pattern – when the pattern of disruption begins it’s difficult to change the end result. But when companies follow the siren’s song of their upmarket customers it doesn’t necessarily mean all the other conditions that facilitate disruption have been satisfied. Just one.

What actually enables disruption – an Extendable Core

In 2012, Clay Christensen and I published an article in the Harvard Business Review discussing how to forecast the extent to which disruption would impact large businesses. To any sort of recommendation, we had to be pretty prescriptive about what actually drives disruption. So we spent a lot of time discussing what we called the extendable core.

The extendable core of a disruptive business is the technology or business model innovation that allows a disruptive entrant to enter a market and scale up their operations in ways that incumbent players can’t replicate. It’s a way of operating that allows them to improve their product or service but maintain an intrinsic structural advantage.

Originally, SaaS companies found their extendable core in multi-tenant cloud architectures. They could write code once, deploy it to infrastructure they purchase at scale, and manage it in a more efficient model. It wasn’t just the revenue model of subscription – anyone in the license software world could have changed the billing process for their products.

When Marc Benioff coupled his subscription software with a means of delivering software that made it cheaper and easier to manage, he hit the disruptive home run out of the park. His extendable core allowed him to deliver basic software to overlooked members of the market (small and medium sized businesses that couldn't have shouldered the burden of high implementation costs). But the business' extendable core also provided the same cost and service advantages as he slowly crept upmarket. As he added features and functionality to compete with offerings like Siebel CRM, he still maintained an intrinsically advantaged position.

Textbook disruption.

Low Cost Doesn’t Mean Disruption

There is a large difference between price competition and disruption. Consider economy hotels.

Why? Any traveler can attest that no one really needs the luxury that brands like the Ritz, the Four Seasons, or even the Marriott offer most customers. What most people truly need when traveling is a bed and a lock on the door to make certain your goods aren't stolen by the random marauder. Everything else is bonus.

Because millions of travelers choose to opt out of the luxury options available, a slew of options exist for the more fiscally conscious traveler such as Econolodge, Holiday Inn Express, and so many more. But just because those hotels serve downmarket customers at a lower price point doesn't make them disruptive. It just makes them cheaper.

The reason? Each of the low cost vendors share the same basic business model as their upmarket competitors. They own and manage a physical inventory of rooms. Because the underlying foundation is similar, for each of the economy hotels to move upmarket they must adopt the same cost structures as their upmarket competitors. As they add the luxurious spas, pools, and restaurants, they lose their ability to under-price their competitors -- effectively losing their competitive advantage.

When Salesforce adopted a multi-tenant cloud model, they changed the game. They could improve their product, add functionality, build their sales organization, and still maintain many advantages that traditional on-premise software vendors could not compete with.

That extendable core is what made their inevitable victory so perfectly predictable.

Companies without this core can still carve out strong positions. Their entry into markets, however, simply can't be trumpeted as the inevitable downfall / disruption of their upmarket brethren. Just because Xero is cheaper than FinancialForce, doesn't mean that FinancialForce is being disrupted. They could be out-producted, out-executed, out-marketed, or out-maneuvered... but they won't be disrupted.

In today's SaaS landscape, there are definitely some disruptive entrants (e.g., Zenefits with a profit model that enables the company to subsidize free software). But there are also numerous examples of simple price competition (e.g., Zoho). And when you're managing a business, it's vital that you know the difference.

Three implications for the SaaS CEO

If the cycle of price pressure in technology isn't resulting necessarily from disruption, the question is what does that mean for SaaS CEOs? With an eye towards three things, this can actually be quite empowering.

1) Know the Competition’s Business Model

If disruption finds its roots in being able to sustainably scale an advantaged position, knowing the strength of your competitors (and your own) business model is key. If you’re a burgeoning SaaS executive, it’s your job to know how your competitors operate. Understand their profit model and their technological foundation.

If you have someone nipping at your ankles you need to be aware whether they're playing the same game as you, or if they're playing a different one. What about an entrants model would allow them to maintain a cost or quality advantage over as they scale.

For example, just because Workday is selling larger and more complex HCM contracts in the cloud along with the bread and butter contracts that helped them grow through their IPO, doesn't mean that an entrant can just walk in and steal their base. But they should keep an eye out for Microsoft, Netsuite, and FinancialForce, who are all trying to win greater share of the ERP market by offering deep integration with the front office applications they own.

If you have someone nipping at your ankles you need to be aware whether they're playing the same game as you, or if they're playing a different one. What about an entrants model would allow them to maintain a cost or quality advantage over as they scale.

For example, just because Workday is selling larger and more complex HCM contracts in the cloud along with the bread and butter contracts that helped them grow through their IPO, doesn't mean that an entrant can just walk in and steal their base. But they should keep an eye out for Microsoft, Netsuite, and FinancialForce, who are all trying to win greater share of the ERP market by offering deep integration with the front office applications they own.

Keep an eye out for new technologies, programming styles, or business models. Ask very deep questions when someone emerges like Zenefits giving your core product away for free. The key is to dig deep and understand whether these competitors can keep their position as they move upmarket.

2) Pursue Different Models for Different Customer Segments

Being disrupted is a terrible thing. When it starts in reality, you can't expect to hold the low end of your market without a different model. But when you're facing simple price competition - as is the case in most SaaS environments - part of the challenge is ensuring you address your different types of customers with the sustainable models.

As young technology firms add the features and functionality to appeal to large enterprises, it’s enticing to increase focus on winning contracts in that segment. It can be a grind to sell 30 contracts at 10K in annual value each to medium-sized businesses. To those businesses, the 10K is often a large commitment. That commitment drives difficulty in the sales process. It’s often easier to trade that high volume, lower value, focus for a focus on lumpier (but far more valuable) enterprise sales where your average contract value may be 300K. Each contract in that segment might drive 30 times the revenue but only be 15 times as complex to close, meaning the overall job is easier.

But just because SMB and mid-market sales are a grind doesn’t mean they’re not worthwhile. The chairman of Taiwan Semiconductor once said, US CEOs love to talk about improving margin, but “so far I have not found a single bank that accepts deposits denominated in ratios. Banks only take currency.” He advocated pursuing any ROI positive sale and simply building piles of cash. If you have a population of customers that clamor from your services, it can be quite lucrative to manage different go-to-market models for those segments.

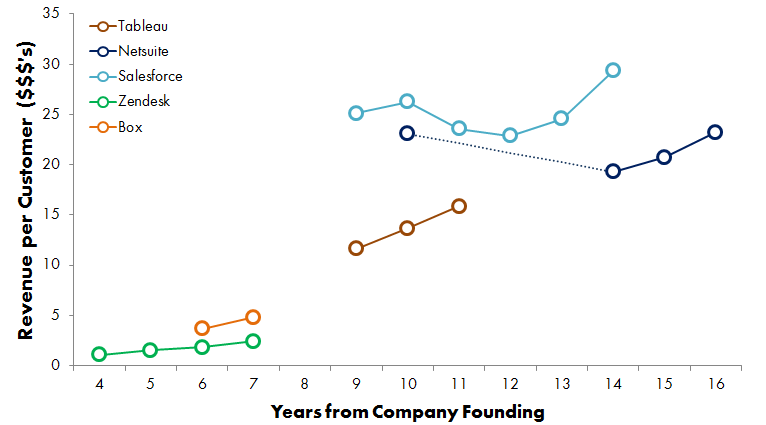

Both Netsuite and Salesforce.com represent shining examples of this practice. Each is driving ever larger contracts in large enterprises and corporate subsidiaries around the globe while continuing to grow their volume base of customers. It requires true discipline and a willingness to do things differently for different customer segments. But with the right sales ops team and good channel and ecosystem, it’s definitely possible.*

Figure 2: Estimated Recent Netsuite and Salesforce Revenue per Customer1

3) Listen to Everyone

Disruption sneaks up on those that stop listening. And more specifically, it sneaks up on those that stop listening to ALL of their customers. Even as your business builds capabilities and breaks into new segments of the market, keep listening across your portfolio. Understand why new products appeal to different members of your customer base and respond accordingly.

Andy Grove famously said that only the paranoid survive. He’s right. If you’re not fearful of the types of businesses that are starting to appeal to even your least valuable customers, you’re creating a chink in your armor. Anyone can execute you out of your pole position if you give them the opportunity.

______

1 Customer count estimates for Salesforce.com derived from Jeff Grosse. Should be directionally correct, though not perfect.

*The added benefit to not retreating from your base is that you can often use your volume to improve your ecosystem. Channel partners and ISVs flock to platforms with high numbers of potential customers. When you have volume, you’ll find yourself with extensions to your solutions that go a long way in defending all segments of your market.